Five years of Digital Asset's adoption (did you know?) is now trickling down to consumers.

Last week on Canton Builders Spotlight, @ShaulKfir joined us. He's the Co-Founder of @digitalasset, the team behind the technology that powers @CantonNetwork, and one of the original co-authors of libSNARK.

If you've seen headlines about institutions adopting Canton, Shaul's work is a major reason it's possible.

Our major takeaway from the interview is that Canton's institutional foundation, of which elements have been quietly being adopted by institutions for 5 years, is now appearing in retail apps and use cases. Here's some of what we covered:

They’re actually Mr. Miyagi-ing crypto into TradFi

Shaul prefers the Mr. Miyagi analogy to the Trojan Horse one that’s being used these days.

Institutions have been adopting Digital Asset's stack since 2020, mostly doing what felt like infrastructure plumbing. Settlement. Collateral management. Tokenized cash. They didn't necessarily understand at the time why it all had to be self-custodial, decentralized, and composable. But the muscle memory built up anyway. Now they're ready for what comes next.

This is the backdrop for the entire recent news cycle. DTCC's decision to use Canton for tokenized collateral, for example, to unlock 24/7 liquidity on over $100 trillion in assets, is the "Mr. Miyagi" muscle memory clicking into place.

How does this trickle down to consumer adoption?

We asked Shaul whether Canton is purely focused on institutions, expecting the standard "for now, but eventually..." answer. He came back faster than that. "No, not at all. It's not purely about institutions. I'll even say at a personal level, not speaking for DA, but for myself, I've never been interested in helping institutions. That's a means to an end."

Then he laid out the model.

"For me, it's all about helping the end users. And that means the retail users, but for the most part, retail users are served by businesses. So I think about it as B2B2C, or maybe network-to-business-to-consumer. Bringing [Canton to] the institutions, and bringing companies in general, is the way to ultimately bring retail users."

The analogy he used: streaming. Mainstream users didn't pick up MP3s or BitTorrent. The mainstream got into streaming when iTunes and Spotify launched. Canton is the compliance-ready private network. The companies building on top of it are the iTunes and Spotify of finance. The retail user shows up when the institutions do.

What the consumer experience starts to look like

Shaul ran through a list of the things he expects to come out of Canton over the next few years that touch consumers directly:

Collateralized lending against tokenized real-world assets. If you're a normal person with assets, your borrowing options today are limited. You can't really shop the rates. However in DeFi, if you own ETH or USDC, every lender in the world is competing for your business and you can pick the best deal. Canton is going to bring that same dynamic to the assets normal people own. Tokenized stocks. Tokenized money market funds. Tokenized real estate. The same DeFi unlock that made ETH useful.

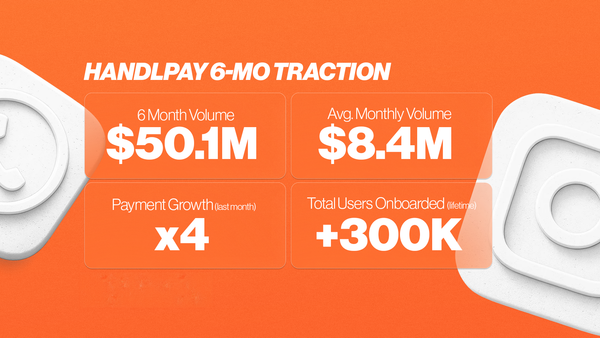

Easy on/off-ramps into yield-bearing products serving stablecoins. This is HandlPay's service offering. If you can let someone with a stablecoin balance move between cash and yield-bearing assets on demand, that's a huge benefit to people who don't have access to the kind of banking that lets you do that today.

Improved UX. He came back to this multiple times. Canton was designed around institutional needs, and it's still behind on ease of use. Improving the consumer experience layer is a big opportunity. His exact phrasing: "Figure out how to get your grandmother to use this."

Reduced exposure to systemic risk: the retail unlock

We asked Shaul directly: are retail users on Canton because of privacy, or because they're betting on institutional adoption?

Both, plus a third thing. As a user, you get access to financial products and rates that used to be reserved for the wealthy. You also get something most people don't think about until it costs them: reduced exposure to systemic risk.

He brought up 2008 and the pension funds that were wiped out by undercollateralized loans. The systems built by crypto are more reliable. If built right, of course.

As a builder, you get to build the consumer layer on top of a network that the largest financial institutions in the world are already settling on.

As a holder, you get a stake in a public-good network that he thinks will run a meaningful portion of global finance in twenty years.

What do the “major deal” headlines mean for consumers?

When we asked what the major institutional deals we have been seeing in the headlines look like for a consumer downstream, he gave a great example.

He recently moved to Israel, which is heavily dependent on the U.S. economy. The ability for an Israeli company to access local-currency liquidity by locking up tokenized U.S. treasuries on-chain is, in his framing, "a huge boom" to economies that aren't dollar economies.

That benefit compounds down to entrepreneurs, startups, freelancers, and ultimately consumers in those countries."These things will play out over many, many years. I don't think people fully understand yet the giant impact that it'll have."

A note for builders

The next Spotify (or Google or Amazon) of finance is either at seed stage or hasn't been founded yet. The 20-year giants of this space are being built today, by people who can finally take the underlying technology for granted.

There are major opportunities available for the companies that figure out how to make Canton usable for retail.That's why we're on Canton. The trickle-down has started.

Can your social media username accept crypto & card payments yet?