Stablecoins Have Already Won & The Numbers are Brutal

While regulators debated and banks ran pilots, suddenly, stablecoins became the world's dominant payment rail.

The revolution is complete.

You're probably already using stablecoins and do not even realize it.

Stablecoins processed $33 trillion in 2025, a 72% increase from 2024. They eclipsed Visa and Mastercard's combined volume ($23.7 trillion in 2025) and handled roughly a third of the entire U.S. ACH system's transaction flow which was $88-92 trillion in 2025.

Galaxy Digital predicts stablecoins will surpass ACH in 2026.

For those who don't understand what this means, ACH (Automated Clearing House) is the U.S. electronic payment network that processes direct deposits, bill payments, tax refunds, and business-to-business transfers.

It's essentially the backbone of American domestic payments.

Market cap exploded from $205 billion in January 2025 to $318 billion by January 2026.

Emerging Markets Led the Revolution

While developed markets debated frameworks, billions of people in emerging markets simply adopted the better technology.

Nigeria: $24 billion in annual stablecoin flows. 26 million users (12% of the population). Nigerian exchanges now quote prices in USDT by default.

Argentina: $93.9 billion in stablecoin value in 2025. With 140% inflation and the peso down 90% since 2020, stablecoins represent 3% of the entire M1 money supply. People pay rent and receive salaries in USDT.

Turkey: $63 billion in stablecoin payments (3.7% of GDP). With the lira down 80% since 2018, merchants accept digital dollars for B2B transactions.

Brazil: $318.8 billion (one-third of all Latin American crypto activity!)

The Remittance System Collapsed Overnight

Traditional remittances charge 6.65% on average for a $200 transfer. Sub-Saharan Africa pays 7.9%. Transfers take 3-7 days.

The old system is dead. Though traditional remittance companies are aware of this and are working to penetrate this market via collaborations and acquisitions.

Ether's Profit is Absurd

Over $10 billion profit in the first nine months of 2025 alone. That's more than Bank of America ($8.9B) and rivals Goldman Sachs ($12.56B), with only 150 employees.

Tether now holds $135 billion in U.S. Treasuries, making it the 17th largest holder globally, ahead of South Korea. It serves 500 million users with $174 billion USDT in circulation.

Meanwhile:

- Visa debuted stablecoin settlement in December 2025

- Standard Chartered and Amazon are exploring launches

- $USDC transaction volume ($18.3T) overtook USDT ($13.3T) in 2025, despite smaller market cap

Regulation Accelerated Adoption

The GENIUS Act passed in July 2025, establishing the first comprehensive U.S. framework for payment stablecoins under FDIC supervision. The EU's MiCA came into full effect. Hong Kong passed its Stablecoin Bill. Twelve countries introduced frameworks by mid-2025.

Why Stablecoins Won, Its Obvious

- Faster: Instant vs 3-7 days

- Cheaper: 0.1-2% vs 6-8% fees

- More stable: USD vs currencies losing 80-90% of value

- More accessible: Smartphone vs bank account & physical branch

Its Time For Consolidation Now

The next battleground is user experience especially for B2C. Solutions that abstract away blockchain complexity will capture mass adoption.

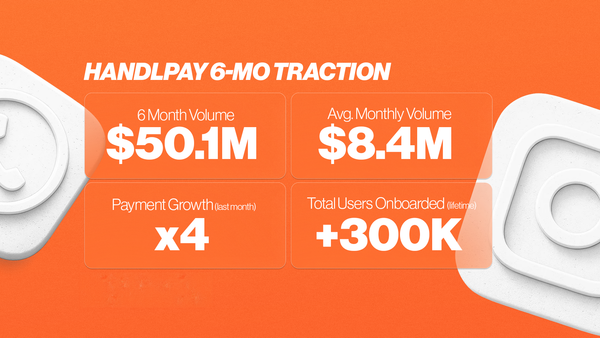

The winners will be platforms that make hundreds of stablecoins feel like one seamless balance, where users never think about routing, bridging, or which chain they're on such as with HandlPay.

We're building cross-chain aggregation, automatic pooling of received payments, and frictionless sending across any network.

The revolution already happened. Now comes the race to make it invisible

Can your social media username accept crypto & card payments yet?